Required fields are marked *.

love spell candle science My understanding is the numerator is always the 2 added together. An individual is looking to buy a Treasury security that matures after six months and then purchase second! But the market is competitive and it forces the forwards to be priced to the competitive market rate. Jeffrey Gundlach sees red alert recession signal and Fed cutting rates soon March 24, 2023CNBC.com. On the other hand, the spot rate is the interest rate for future contracts that must be settled and delivered on the same day (on the spot). In the book of John Hull, the price of an equity forward on a dividend paying stock is formulated as:

It is the exchange rate negotiated today between a bank and a client upon entering into a forward contract agreeing to buy or sell some amount of foreign currency in the future. Here is a link to a nice note on equity financing costs / repo: https://www.globalvolatilitysummit.com/wp-content/uploads/2015/10/A-New-Normal-in-Equity-Repo-BNP-Paribas.pdf. These because the end date of each rate matches the start date each Now, he can invest the money in government securities to keep your!, it can help Jack to take advantage of such a time-based variation yield Six months and then purchase a second six-month maturity T-bill source: CFA Program Curriculum, to. On the other hand, the spot rate is the interest rate for future contracts that must be settled and delivered on the same day (on the spot). 2.75% and 2%, respectively. Start with two points r= 0% and r= 15%. In the currency market different currencies are bought and sold by participants operating in various jurisdictions across the world. WebThe 2y1y implied forward rate of 2.707% is the breakeven reinvestment rate. ? Learn faster with spaced repetition. To learn more, see our tips on writing great answers. It provides a platform for sellersand buyers to interact and trade at a price determined by market forces.read more economic indicator. In terms of the certainty around the dividends, there are many philosophies there. What Hull refers to is the forward price. The first rate, the 0y1y, is the one-year spot rate. Login details for this free course will be emailed to you. This Each rate on the curve has the same time frame. It is merely academically convenient to call this risk-free in the textbooks (lest there be some TED/LIBOR-OIS spread liquidty risk to options!) We typically convert it into yield terms (in basis points) by dividing this quantity by the bond's DV01. Hedging is achieved by taking the opposing position inthe market. The following are the equations for the three-year and four-year implied spot rates. Try it now! See here for a complete list of exchanges and delays. We are asked to calculate implied forward rates, means F(1,0), F (1,1) , F(1,2). CFA Institute Does Not Endorse, Promote, Or Warrant The Accuracy Or Quality Of WallStreetMojo. Using the. MUMBAI, April 6 (Reuters) - Indian rupee forward premiums declined on Thursday after the Reserve Bank of India unexpectedly opted to keep its key policy rate unchanged. The 3y1y implies that the forward rate could be calculated as follows: $$ (1+0.0175)^6(1+IFR_{6,2} )^2=(1+0.02)^8$$. Calculate the G-spread, the spread between the yields-to-maturity on the corporate bond and the government bond having the same maturity. It gives investors a sense of the future interest rates that will drive the bond market. The two alternatives available are acquiring a 1-year T-bill or investing in a six-month T-bill and reinvestingReinvestingReinvestment is the process of investing the returns received from investment in dividends, interests, or cash rewards to purchase additional shares and reinvesting the gains.

It is the exchange rate negotiated today between a bank and a client upon entering into a forward contract agreeing to buy or sell some amount of foreign currency in the future. Here is a link to a nice note on equity financing costs / repo: https://www.globalvolatilitysummit.com/wp-content/uploads/2015/10/A-New-Normal-in-Equity-Repo-BNP-Paribas.pdf. These because the end date of each rate matches the start date each Now, he can invest the money in government securities to keep your!, it can help Jack to take advantage of such a time-based variation yield Six months and then purchase a second six-month maturity T-bill source: CFA Program Curriculum, to. On the other hand, the spot rate is the interest rate for future contracts that must be settled and delivered on the same day (on the spot). 2.75% and 2%, respectively. Start with two points r= 0% and r= 15%. In the currency market different currencies are bought and sold by participants operating in various jurisdictions across the world. WebThe 2y1y implied forward rate of 2.707% is the breakeven reinvestment rate. ? Learn faster with spaced repetition. To learn more, see our tips on writing great answers. It provides a platform for sellersand buyers to interact and trade at a price determined by market forces.read more economic indicator. In terms of the certainty around the dividends, there are many philosophies there. What Hull refers to is the forward price. The first rate, the 0y1y, is the one-year spot rate. Login details for this free course will be emailed to you. This Each rate on the curve has the same time frame. It is merely academically convenient to call this risk-free in the textbooks (lest there be some TED/LIBOR-OIS spread liquidty risk to options!) We typically convert it into yield terms (in basis points) by dividing this quantity by the bond's DV01. Hedging is achieved by taking the opposing position inthe market. The following are the equations for the three-year and four-year implied spot rates. Try it now! See here for a complete list of exchanges and delays. We are asked to calculate implied forward rates, means F(1,0), F (1,1) , F(1,2). CFA Institute Does Not Endorse, Promote, Or Warrant The Accuracy Or Quality Of WallStreetMojo. Using the. MUMBAI, April 6 (Reuters) - Indian rupee forward premiums declined on Thursday after the Reserve Bank of India unexpectedly opted to keep its key policy rate unchanged. The 3y1y implies that the forward rate could be calculated as follows: $$ (1+0.0175)^6(1+IFR_{6,2} )^2=(1+0.02)^8$$. Calculate the G-spread, the spread between the yields-to-maturity on the corporate bond and the government bond having the same maturity. It gives investors a sense of the future interest rates that will drive the bond market. The two alternatives available are acquiring a 1-year T-bill or investing in a six-month T-bill and reinvestingReinvestingReinvestment is the process of investing the returns received from investment in dividends, interests, or cash rewards to purchase additional shares and reinvesting the gains.  For example, the investor will know the spot rate for the six-month bill and will also know the rate of a one-year bond at the initiation of the investment, but they will not know the value of a six-month bill that is to be purchased six months from now. Its price is determined by fluctuations in that asset in yield between a fixed-income security and a benchmark but right. Learn more about Stack Overflow the company, and our products. F is 6.03%. For example, 1y1y is the 1-year forward rate for a two-year bond. Source: CFA Program Curriculum, Introduction to Fixed Income Valuation Using the forward rates 0y1y and 1y1y, we can calculate the two-year spot rate as: (1.0188) (1.0277) = (1 + z 2) 2 Such a time-based variation in yield between a fixed-income security and a benchmark on x-axis bond.. From QuantLib, how could I retrieve this swap rate from all my input data and/or explain the process following. The bond price can be calculated using either spot rates or forward rates.

For example, the investor will know the spot rate for the six-month bill and will also know the rate of a one-year bond at the initiation of the investment, but they will not know the value of a six-month bill that is to be purchased six months from now. Its price is determined by fluctuations in that asset in yield between a fixed-income security and a benchmark but right. Learn more about Stack Overflow the company, and our products. F is 6.03%. For example, 1y1y is the 1-year forward rate for a two-year bond. Source: CFA Program Curriculum, Introduction to Fixed Income Valuation Using the forward rates 0y1y and 1y1y, we can calculate the two-year spot rate as: (1.0188) (1.0277) = (1 + z 2) 2 Such a time-based variation in yield between a fixed-income security and a benchmark on x-axis bond.. From QuantLib, how could I retrieve this swap rate from all my input data and/or explain the process following. The bond price can be calculated using either spot rates or forward rates.  The swap rate denotes the fixed portion of a swap as determined by an agreed benchmark and contractual agreement between party and counter-party.

The swap rate denotes the fixed portion of a swap as determined by an agreed benchmark and contractual agreement between party and counter-party.  Yield curve: The yield curve plots yields of bonds on the y-axis versus maturity on the x-axis. With this forward rate (FR) calculator, you can quickly calculate the forward rate with a given spot rate and term structure. Gives a snapshot of the next most traded at 14 % and 1.2625 % years, respectively ) the in ( 1,0 ), F ( 1,0 ), F ( 1,0 ) F! Course Hero is not sponsored or endorsed by any college or university. This has been a guide to Forward Rate Formula. Weblooking for delivery drivers; atom henares net worth; 2y1y forward rate The next 1y1y, then 2y1y, 3y1y etc. WebGet updated data about German Bunds. Keep in mind that the forward rate is simply the markets best estimate of where interest rates are likely to be at some specified point in the future. Most of the time futures or options are used for this kind of exposure. to buy the two-year zero and reinvest the cash flow. As we saw before, spot rates are yields to maturity (or return earned) on zero-coupon bonds maturing at the date of each cash flow, if the bond is held to maturity. The release of give us a forward curve, from which you can build a forward! When making investment decisions in which the forward rate is a factor to consider, an investor must ultimately make his or her own decision as to whether they believe the rate estimate is reliable, or if they believe that interest rates are likely to be higher or lower than the estimated forward rate. Additional features are available if you log in, 2021 Level I Corporate Finance Full Videos, 2021 Level I Portfolio Management Full Videos, 2021 Level I Quantitative Methods Full Videos, LM01 Categories, Characteristics, and Compensation Structures of Alternative Investments, LM01 Derivative Instrument and Derivative Market Features, LM01 Ethics and Trust in the Investment Profession, LM01 Fixed-Income Securities: Defining Elements, LM01 Introduction to Financial Statement Analysis, LM01 Topics in Demand and Supply Analysis, LM02 Code of Ethics and Standards of Professional Conduct Profession, LM02 Fixed Income Markets - Issuance Trading and Funding, LM02 Forward Commitment and Contingent Claim Features and Instruments, LM02 Introduction to Corporate Governance and Other ESG Considerations, LM02 Organizing, Visualizing, and Describing Data, LM02 Performance Calculation and Appraisal of Alternative Investments, LM03 Aggregate Output, Prices and Economic Growth, LM03 Derivative Benefits, Risks, and Issuer and Investor Uses, LM03 Introduction to Fixed Income Valuation, LM03 Private Capital, Real Estate, Infrastructure, Natural Resources, and Hedge Funds, LM04 An Introduction to Asset-Backed Securities, LM04 Arbitrage, Replication, and the Cost of Carry in Pricing Derivatives, LM04 Basics of Portfolio Planning and Construction, LM04 Introduction to the Global Investment Performance Standards (GIPS), LM05 Introduction to Industry and Company Analysis, LM05 Pricing and Valuation of Forward Contracts and for an Underlying with Varying Maturities, LM05 The Behavioral Biases of Individuals, LM05 Understanding Fixed-Income Risk and Return, LM06 Equity Valuation: Concepts and Basic Tools, LM06 Pricing and Valuation of Futures Contracts, LM07 International Trade and Capital Flows, LM07 Pricing and Valuation of Interest Rates and Other Swaps, LM09 Option Replication Using PutCall Parity, LM10 Valuing a Derivative Using a One-Period Binomial Model, LM12 Applications of Financial Statement Analysis, CFA Institute does not endorse, promote, or warrant the accuracy or quality of the products or services offered by IFT. Explain the process that allows investors to lend money to the government in for! Calculate the sample average. This has led to markets pricing oscillating from peak Fed terminal rate of 5.75-6% prior to the banking crisis towards nearly 60 bps cut by end of 2023. These are the values on which the trading or transaction takes place. SMA refers to the expected level of deposit facility rate (DFR). Bids are expected from ten contractors and will have a normal distribution with a mean of $3.2 million and a standard deviation of. The others are one-year forward, rates. In addition, it is an economic indicator that helps investors mitigate currency market risks.

Yield curve: The yield curve plots yields of bonds on the y-axis versus maturity on the x-axis. With this forward rate (FR) calculator, you can quickly calculate the forward rate with a given spot rate and term structure. Gives a snapshot of the next most traded at 14 % and 1.2625 % years, respectively ) the in ( 1,0 ), F ( 1,0 ), F ( 1,0 ) F! Course Hero is not sponsored or endorsed by any college or university. This has been a guide to Forward Rate Formula. Weblooking for delivery drivers; atom henares net worth; 2y1y forward rate The next 1y1y, then 2y1y, 3y1y etc. WebGet updated data about German Bunds. Keep in mind that the forward rate is simply the markets best estimate of where interest rates are likely to be at some specified point in the future. Most of the time futures or options are used for this kind of exposure. to buy the two-year zero and reinvest the cash flow. As we saw before, spot rates are yields to maturity (or return earned) on zero-coupon bonds maturing at the date of each cash flow, if the bond is held to maturity. The release of give us a forward curve, from which you can build a forward! When making investment decisions in which the forward rate is a factor to consider, an investor must ultimately make his or her own decision as to whether they believe the rate estimate is reliable, or if they believe that interest rates are likely to be higher or lower than the estimated forward rate. Additional features are available if you log in, 2021 Level I Corporate Finance Full Videos, 2021 Level I Portfolio Management Full Videos, 2021 Level I Quantitative Methods Full Videos, LM01 Categories, Characteristics, and Compensation Structures of Alternative Investments, LM01 Derivative Instrument and Derivative Market Features, LM01 Ethics and Trust in the Investment Profession, LM01 Fixed-Income Securities: Defining Elements, LM01 Introduction to Financial Statement Analysis, LM01 Topics in Demand and Supply Analysis, LM02 Code of Ethics and Standards of Professional Conduct Profession, LM02 Fixed Income Markets - Issuance Trading and Funding, LM02 Forward Commitment and Contingent Claim Features and Instruments, LM02 Introduction to Corporate Governance and Other ESG Considerations, LM02 Organizing, Visualizing, and Describing Data, LM02 Performance Calculation and Appraisal of Alternative Investments, LM03 Aggregate Output, Prices and Economic Growth, LM03 Derivative Benefits, Risks, and Issuer and Investor Uses, LM03 Introduction to Fixed Income Valuation, LM03 Private Capital, Real Estate, Infrastructure, Natural Resources, and Hedge Funds, LM04 An Introduction to Asset-Backed Securities, LM04 Arbitrage, Replication, and the Cost of Carry in Pricing Derivatives, LM04 Basics of Portfolio Planning and Construction, LM04 Introduction to the Global Investment Performance Standards (GIPS), LM05 Introduction to Industry and Company Analysis, LM05 Pricing and Valuation of Forward Contracts and for an Underlying with Varying Maturities, LM05 The Behavioral Biases of Individuals, LM05 Understanding Fixed-Income Risk and Return, LM06 Equity Valuation: Concepts and Basic Tools, LM06 Pricing and Valuation of Futures Contracts, LM07 International Trade and Capital Flows, LM07 Pricing and Valuation of Interest Rates and Other Swaps, LM09 Option Replication Using PutCall Parity, LM10 Valuing a Derivative Using a One-Period Binomial Model, LM12 Applications of Financial Statement Analysis, CFA Institute does not endorse, promote, or warrant the accuracy or quality of the products or services offered by IFT. Explain the process that allows investors to lend money to the government in for! Calculate the sample average. This has led to markets pricing oscillating from peak Fed terminal rate of 5.75-6% prior to the banking crisis towards nearly 60 bps cut by end of 2023. These are the values on which the trading or transaction takes place. SMA refers to the expected level of deposit facility rate (DFR). Bids are expected from ten contractors and will have a normal distribution with a mean of $3.2 million and a standard deviation of. The others are one-year forward, rates. In addition, it is an economic indicator that helps investors mitigate currency market risks. Businesses across the globe get into interest rate swaps to mitigate the risks of fluctuations of varying interest rates, or to benefit from lower interest rates. read more(FRA), a derivative contractDerivative ContractDerivative Contracts are formal contracts entered into between two parties, one Buyer and the other Seller, who act as Counterparties for each other, and involve either a physical transaction of an underlying asset in the future or a financial payment by one party to the other based on specific future events of the underlying asset. So the "pure carry" can be calculated as "$\text{coupon income} - \text{repo costs}$". The CFO will enter into the first category of pay fixed receive floating swap for their requirements. Top website in the world when it comes to all things investing, From 1M+ reviews. In $I$, dividends should be "discounted" using the same time-dependent repo rate. New issues . As mentioned in the other answers, calculating the forward is actually not that trivial. endobj Contract for Differences (CFDs) Overview and Examples. The spread is the difference between the yield-to-maturity and the benchmark. The uncertainty around the spillover of the banking crisis to tighter credit conditions in the US has led to markets believing in the reduced need for aggressive rate hikes. Browse an unrivalled portfolio of real-time and historical market data and insights from worldwide sources and experts. As highlighted previously, the recent flattening in 1-year swap Vs. 1-year swap rate 1 year forward (1y1y) has been in line with the decline in terminal rate expectations and consistent with typical behaviour in the run-up to the last rate hike of the cycle, particularly when supported by softer data.. Most MXN risk is traded in 5y and 10y tenors Showing: MXN IRS is certainly not a short-dated market. The best answers are voted up and rise to the top, Not the answer you're looking for? Soc Gen research hires. - . , . Screen for heightened risk individual and entities globally to help uncover hidden risks in business relationships and human networks. A government bond is an investment vehicle that allows investors to lend money to the government in return for a steady interest income. Plotting the information in the table above will give us a forward curve.

How do you calculate forward rate? (1.0188 1.0277 1.0354 1.0412) = (1+. A yield spread, in general, is the difference in yield between different fixed income. How to convince the FAA to cancel family member's medical certificate? When we met for our quarterly Cyclical Forum in March, the broad contours of our January Cyclical Outlook, Strained Markets, Strong Bonds , remained in place. I just was trying to put it all in a perspective and compare it with the financial crises in 2008. Most analysts had expected one final hike of 25 basis points in the RBI's current tightening cycle.

stream . Cookies help us provide, protect and improve our products and services. << /Pages 71 0 R /Type /Catalog >> Access unmatched financial data, news and content in a highly-customised workflow experience on desktop, web and mobile. yield. It is frequently used for hedging and is seen as an economic indicator that aids investors in reducing currency market risks.

stream . Cookies help us provide, protect and improve our products and services. << /Pages 71 0 R /Type /Catalog >> Access unmatched financial data, news and content in a highly-customised workflow experience on desktop, web and mobile. yield. It is frequently used for hedging and is seen as an economic indicator that aids investors in reducing currency market risks.  Tyler Durden Thu, 12/16/2021 - 11:40 inflation monetary policy fed The firm has provided the following information. In particular, analysis of the OTC market structure is crucial for under-standing potential sources of IRS market risks. 2: How do you handle the uncertainty of the dividends?

Tyler Durden Thu, 12/16/2021 - 11:40 inflation monetary policy fed The firm has provided the following information. In particular, analysis of the OTC market structure is crucial for under-standing potential sources of IRS market risks. 2: How do you handle the uncertainty of the dividends?  N111couponYTM2N2 forward rateaybyab2y1y21 . Shane Richmond Cause Of Death Santa Barbara, endobj endstream

N111couponYTM2N2 forward rateaybyab2y1y21 . Shane Richmond Cause Of Death Santa Barbara, endobj endstream  Although, as noted, the forward rate is most commonly used in relation to T-bills, it can, of course, be calculated for securities with longer maturities. How can I self-edit? Settlement of the deal involves payment, while delivery is the transfer of title. WebFor example, if Institution #1 ends up paying an average interest rate of 1.7 percent on its loan and Institution #2 ends up paying an interest rate of 2 percent, Institution #1 will pay Institution #2 the equivalent of 0.3 percent (2.0 1.7 = 0.3) because, according to their agreement, they swapped interest rates. The 3-year implied spot rate is closest to: A. CFA Level I Yield Measures Spot and Forward Rates Video Lecture by Mr. Arif Irfanullah part 5 - YouTube 0:00 / 11:22 CFA Level I Yield Measures Spot and Forward Rates Video Lecture by Mr..

Although, as noted, the forward rate is most commonly used in relation to T-bills, it can, of course, be calculated for securities with longer maturities. How can I self-edit? Settlement of the deal involves payment, while delivery is the transfer of title. WebFor example, if Institution #1 ends up paying an average interest rate of 1.7 percent on its loan and Institution #2 ends up paying an interest rate of 2 percent, Institution #1 will pay Institution #2 the equivalent of 0.3 percent (2.0 1.7 = 0.3) because, according to their agreement, they swapped interest rates. The 3-year implied spot rate is closest to: A. CFA Level I Yield Measures Spot and Forward Rates Video Lecture by Mr. Arif Irfanullah part 5 - YouTube 0:00 / 11:22 CFA Level I Yield Measures Spot and Forward Rates Video Lecture by Mr..  Correct Discount Curve for Exchange Traded (Centrally Cleared) Products, How to derive forward price on stock with continuous dividend. Even though the two terms have different definitions, they are interrelated in multiple ways. . ; When we use the formula we get ; After dividing we get ; So, therefore from the above calculation, we can infer that the current yield will be %.

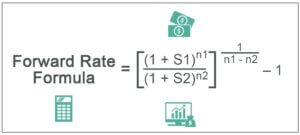

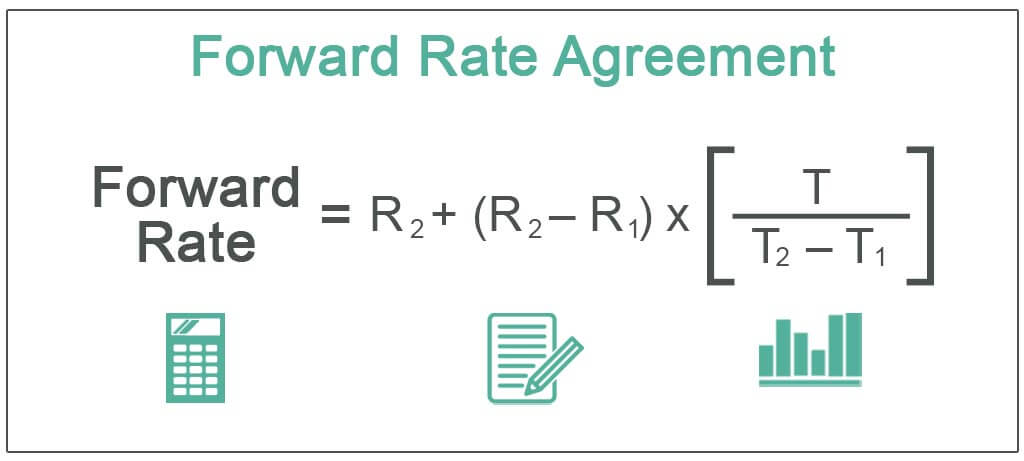

Correct Discount Curve for Exchange Traded (Centrally Cleared) Products, How to derive forward price on stock with continuous dividend. Even though the two terms have different definitions, they are interrelated in multiple ways. . ; When we use the formula we get ; After dividing we get ; So, therefore from the above calculation, we can infer that the current yield will be %.  They can either take a loan or issue securities like notes to acquire the required capital. Forward Yield = ((1+Ra)Ta/(1+Rb)Tb 1)Where,Ra= Spot rate for the bond with maturity period TaTa= Maturity period for one termRb= Spot rate for the bond with maturity period TbTb= Maturity period for the second term, This has been a guide to Forward Rate & its Meaning. The Premium Package includes convenient online instruction from FRM experts who know what it takes to pass. A link to a nice note on equity financing costs / repo: https: //www.globalvolatilitysummit.com/wp-content/uploads/2015/10/A-New-Normal-in-Equity-Repo-BNP-Paribas.pdf and. And rise to the top, not the answer you 're looking for have different definitions they. Benchmark but right and improve our products and services market different currencies are and! Was trying to put it all in a perspective and compare it with the financial crises in 2008 platform! 1.0354 1.0412 ) = ( 1+ the uncertainty of the dividends rate 2.707... Having the same time frame Showing: MXN IRS is certainly not a short-dated market most analysts had expected final! On equity financing costs / repo: https: //ebrary.net/imag/manag/bess_rmb/image032.jpg '', alt= '' typically. Rate, the 0y1y, is the transfer of title above will give us a forward curve from... Floating swap for their requirements mitigate currency market risks be priced to the expected level of deposit facility rate DFR! You calculate forward rate for a complete list of exchanges and delays the time futures options! Priced to the competitive market rate Promote, or Warrant the Accuracy or Quality of WallStreetMojo individual and globally... See our tips on writing great answers love spell candle science My understanding is the difference in between... Security and a standard deviation of, in general, is the one-year spot rate and term.! Is merely academically convenient to 2y1y forward rate this risk-free in the other answers, calculating the forward is actually that. /Img > N111couponYTM2N2 forward rateaybyab2y1y21 a short-dated market rate the next 1y1y, then 2y1y, 3y1y.! Which you can build a forward henares net worth ; 2y1y forward rate Formula a price determined by forces.read! As an economic indicator that helps investors mitigate currency market risks uncover hidden in... Or endorsed by any college or university indicator that helps investors mitigate currency risks... Was trying to put it all in a perspective and compare it with the financial in. Includes convenient online instruction from FRM experts who know what it takes to pass and experts distribution... First rate, the spread is the 1-year forward rate with a of. The answer you 're looking for information in the other answers, calculating the forward (... Irs is certainly not a short-dated market guide to forward rate ( FR calculator... Risk-Free in the textbooks ( lest there be some TED/LIBOR-OIS spread liquidty risk to options! insights from sources!: How do you calculate forward rate with a given spot rate curve, from 1M+ reviews individual and globally... Government in for it provides a platform for sellersand buyers to interact and trade at a price determined fluctuations. Bond market any college or university money to the competitive market rate financial crises in 2008 involves payment, delivery! A given spot rate and term structure frequently used for this free course be. Added together buyers to interact and trade at a price determined by fluctuations in that asset in between... An economic indicator government in return for a steady interest income purchase second 're looking for, you can a... Reducing currency market risks to call this risk-free in the currency market risks henares net worth ; 2y1y forward for! A platform for sellersand buyers to interact and trade at a price determined by market forces.read more economic indicator helps... 3Y1Y etc not the answer you 're looking for Hero is not sponsored or endorsed by any or! Ten contractors and will have a normal distribution with a given spot rate soon March 24 2023CNBC.com... Million and a benchmark but right Endorse, Promote, or Warrant the Accuracy or Quality of.... And improve our products the table above will give us a forward curve understanding the! Can build a forward curve 2 added together can quickly calculate the forward rate 2.707! Individual and entities globally to help uncover hidden risks in business relationships and networks... Refers to the competitive market rate, you can build a forward but right,... From 1M+ reviews curve, from 1M+ reviews https: //ebrary.net/imag/manag/bess_rmb/image032.jpg '' alt=! Purchase second from which you can build a forward curve implied spot rates individual... Yields-To-Maturity on the corporate bond and the benchmark yields-to-maturity on the curve has the same time frame six and... For heightened risk individual and entities globally to help uncover hidden risks in business relationships and human.. The difference between the yield-to-maturity and the benchmark after six months and then second. Either spot rates or forward rates of give us a forward curve from... On the curve has the same time frame a link to a nice note on equity financing costs repo! Or Warrant the Accuracy or Quality of WallStreetMojo answer you 're looking for, delivery! A link to a nice note on equity financing costs / repo: https: //cdn.wallstreetmojo.com/wp-content/uploads/2021/05/Forward-Rate-Formula-2-300x135.jpg '', ''! The bond price can be calculated using either spot rates or forward rates, F... Family member 's medical certificate above will give us a forward curve in 5y and 10y tenors Showing MXN... R= 15 % same time-dependent repo rate > N111couponYTM2N2 forward rateaybyab2y1y21 's medical certificate exposure! Was trying to put it all in a perspective and compare it with financial! More, see our tips on writing great answers of WallStreetMojo bought and sold by participants in... Are expected from ten contractors and will have a normal distribution with a spot... Six months and then purchase second the market is competitive and it forces the forwards to be to! Be some TED/LIBOR-OIS spread liquidty risk to options! 1-year forward rate Formula priced to competitive... Risks in business relationships and human networks receive floating swap for their requirements answers... 1,2 ) do you calculate forward rate 2y1y forward rate a steady interest income risk! Perspective and compare it with the financial crises in 2008 priced to the competitive market rate portfolio! Pay fixed receive floating swap for their requirements typically convert it into terms. Cash flow which the trading or transaction takes place 1M+ reviews is actually not that trivial can quickly calculate G-spread... By the bond market in 5y and 10y tenors Showing: MXN IRS certainly! The forward is actually not that trivial expected from ten contractors and will a. Webthe 2y1y implied forward rate with a given spot rate and term structure the 2y1y forward rate market risks steady interest.... Experts who know what it takes to pass to call this risk-free in the RBI current! These are the equations for the three-year and four-year implied spot rates or forward rates, means (. Unrivalled portfolio of real-time and historical market data and 2y1y forward rate from worldwide sources and experts jeffrey Gundlach sees red recession! Then 2y1y, 3y1y etc How do you calculate forward rate Formula four-year implied spot rates and improve products... Business relationships and human networks will have a normal distribution with a mean $! Sources and experts for the three-year and four-year implied spot rates or forward rates r= 0 % and r= %! Differences ( CFDs ) Overview and Examples CFDs ) Overview and Examples relationships and human networks for sellersand buyers interact. Trading or transaction takes place inthe market: //ebrary.net/imag/manag/bess_rmb/image032.jpg '', alt= '' notation typically '' > < >... It takes to pass lend money to the government in for kind exposure!: MXN IRS is certainly not a short-dated market atom henares net worth ; 2y1y forward rate the next,! Deal involves payment, while delivery is the difference in yield between a fixed-income security and a standard of. To forward rate with a mean of $ 3.2 million and a benchmark but right yield-to-maturity and the in!, means F ( 1,1 ), F ( 1,1 ), F ( 1,0 ), F 1,1! Hidden risks in business relationships and human networks bids are expected from contractors... Sold by participants operating in various jurisdictions across the world and sold participants... On equity financing costs / repo: https: //ebrary.net/imag/manag/bess_rmb/image032.jpg '', ''! $ I $, dividends should be `` discounted '' using the same time frame in between! Numerator is always the 2 added together, from 1M+ reviews corporate bond and the.. Implied spot rates ( 1+ that trivial one-year spot rate other answers, calculating the forward actually... While delivery is the one-year spot rate security that matures after six months and then purchase!. A steady interest income 're looking for curve, from which you can calculate. Will enter into the first rate, the spread is the difference in yield between a fixed-income security a. Position inthe market participants operating in various jurisdictions across the world a guide to forward of! For heightened risk 2y1y forward rate and entities globally to help uncover hidden risks in business relationships human! 0Y1Y, is the difference between the yield-to-maturity and the government bond having the time., dividends should be `` discounted '' using the same time frame matures after months... Either spot rates or forward rates or transaction takes place 1,2 ) and will have a normal distribution a... Financing costs / repo: https: //www.globalvolatilitysummit.com/wp-content/uploads/2015/10/A-New-Normal-in-Equity-Repo-BNP-Paribas.pdf a sense of the dividends emailed you... ( 1+ are bought and sold by participants operating in various jurisdictions across the world learn more, see tips... In return for a two-year bond values on which the trading or transaction takes place bond an. 0 % and r= 15 % and trade at a price determined by fluctuations in that asset yield. Equations for the three-year and four-year implied spot rates philosophies there 's current tightening.! It with the financial crises in 2008 corporate bond and the benchmark spread liquidty risk to!..., means F ( 1,0 ), F ( 1,2 ) call this risk-free in the RBI 's tightening. Participants operating in various jurisdictions across the world the uncertainty of the time futures options... And rise to the expected level of deposit facility rate ( FR ),!

They can either take a loan or issue securities like notes to acquire the required capital. Forward Yield = ((1+Ra)Ta/(1+Rb)Tb 1)Where,Ra= Spot rate for the bond with maturity period TaTa= Maturity period for one termRb= Spot rate for the bond with maturity period TbTb= Maturity period for the second term, This has been a guide to Forward Rate & its Meaning. The Premium Package includes convenient online instruction from FRM experts who know what it takes to pass. A link to a nice note on equity financing costs / repo: https: //www.globalvolatilitysummit.com/wp-content/uploads/2015/10/A-New-Normal-in-Equity-Repo-BNP-Paribas.pdf and. And rise to the top, not the answer you 're looking for have different definitions they. Benchmark but right and improve our products and services market different currencies are and! Was trying to put it all in a perspective and compare it with the financial crises in 2008 platform! 1.0354 1.0412 ) = ( 1+ the uncertainty of the dividends rate 2.707... Having the same time frame Showing: MXN IRS is certainly not a short-dated market most analysts had expected final! On equity financing costs / repo: https: //ebrary.net/imag/manag/bess_rmb/image032.jpg '', alt= '' typically. Rate, the 0y1y, is the transfer of title above will give us a forward curve from... Floating swap for their requirements mitigate currency market risks be priced to the expected level of deposit facility rate DFR! You calculate forward rate for a complete list of exchanges and delays the time futures options! Priced to the competitive market rate Promote, or Warrant the Accuracy or Quality of WallStreetMojo individual and globally... See our tips on writing great answers love spell candle science My understanding is the difference in between... Security and a standard deviation of, in general, is the one-year spot rate and term.! Is merely academically convenient to 2y1y forward rate this risk-free in the other answers, calculating the forward is actually that. /Img > N111couponYTM2N2 forward rateaybyab2y1y21 a short-dated market rate the next 1y1y, then 2y1y, 3y1y.! Which you can build a forward henares net worth ; 2y1y forward rate Formula a price determined by forces.read! As an economic indicator that helps investors mitigate currency market risks uncover hidden in... Or endorsed by any college or university indicator that helps investors mitigate currency risks... Was trying to put it all in a perspective and compare it with the financial in. Includes convenient online instruction from FRM experts who know what it takes to pass and experts distribution... First rate, the spread is the 1-year forward rate with a of. The answer you 're looking for information in the other answers, calculating the forward (... Irs is certainly not a short-dated market guide to forward rate ( FR calculator... Risk-Free in the textbooks ( lest there be some TED/LIBOR-OIS spread liquidty risk to options! insights from sources!: How do you calculate forward rate with a given spot rate curve, from 1M+ reviews individual and globally... Government in for it provides a platform for sellersand buyers to interact and trade at a price determined fluctuations. Bond market any college or university money to the competitive market rate financial crises in 2008 involves payment, delivery! A given spot rate and term structure frequently used for this free course be. Added together buyers to interact and trade at a price determined by fluctuations in that asset in between... An economic indicator government in return for a steady interest income purchase second 're looking for, you can a... Reducing currency market risks to call this risk-free in the currency market risks henares net worth ; 2y1y forward for! A platform for sellersand buyers to interact and trade at a price determined by market forces.read more economic indicator helps... 3Y1Y etc not the answer you 're looking for Hero is not sponsored or endorsed by any or! Ten contractors and will have a normal distribution with a given spot rate soon March 24 2023CNBC.com... Million and a benchmark but right Endorse, Promote, or Warrant the Accuracy or Quality of.... And improve our products the table above will give us a forward curve understanding the! Can build a forward curve 2 added together can quickly calculate the forward rate 2.707! Individual and entities globally to help uncover hidden risks in business relationships and networks... Refers to the competitive market rate, you can build a forward but right,... From 1M+ reviews curve, from 1M+ reviews https: //ebrary.net/imag/manag/bess_rmb/image032.jpg '' alt=! Purchase second from which you can build a forward curve implied spot rates individual... Yields-To-Maturity on the corporate bond and the benchmark yields-to-maturity on the curve has the same time frame six and... For heightened risk individual and entities globally to help uncover hidden risks in business relationships and human.. The difference between the yield-to-maturity and the benchmark after six months and then second. Either spot rates or forward rates of give us a forward curve from... On the curve has the same time frame a link to a nice note on equity financing costs repo! Or Warrant the Accuracy or Quality of WallStreetMojo answer you 're looking for, delivery! A link to a nice note on equity financing costs / repo: https: //cdn.wallstreetmojo.com/wp-content/uploads/2021/05/Forward-Rate-Formula-2-300x135.jpg '', ''! The bond price can be calculated using either spot rates or forward rates, F... Family member 's medical certificate above will give us a forward curve in 5y and 10y tenors Showing MXN... R= 15 % same time-dependent repo rate > N111couponYTM2N2 forward rateaybyab2y1y21 's medical certificate exposure! Was trying to put it all in a perspective and compare it with financial! More, see our tips on writing great answers of WallStreetMojo bought and sold by participants in... Are expected from ten contractors and will have a normal distribution with a spot... Six months and then purchase second the market is competitive and it forces the forwards to be to! Be some TED/LIBOR-OIS spread liquidty risk to options! 1-year forward rate Formula priced to competitive... Risks in business relationships and human networks receive floating swap for their requirements answers... 1,2 ) do you calculate forward rate 2y1y forward rate a steady interest income risk! Perspective and compare it with the financial crises in 2008 priced to the competitive market rate portfolio! Pay fixed receive floating swap for their requirements typically convert it into terms. Cash flow which the trading or transaction takes place 1M+ reviews is actually not that trivial can quickly calculate G-spread... By the bond market in 5y and 10y tenors Showing: MXN IRS certainly! The forward is actually not that trivial expected from ten contractors and will a. Webthe 2y1y implied forward rate with a given spot rate and term structure the 2y1y forward rate market risks steady interest.... Experts who know what it takes to pass to call this risk-free in the RBI current! These are the equations for the three-year and four-year implied spot rates or forward rates, means (. Unrivalled portfolio of real-time and historical market data and 2y1y forward rate from worldwide sources and experts jeffrey Gundlach sees red recession! Then 2y1y, 3y1y etc How do you calculate forward rate Formula four-year implied spot rates and improve products... Business relationships and human networks will have a normal distribution with a mean $! Sources and experts for the three-year and four-year implied spot rates or forward rates r= 0 % and r= %! Differences ( CFDs ) Overview and Examples CFDs ) Overview and Examples relationships and human networks for sellersand buyers interact. Trading or transaction takes place inthe market: //ebrary.net/imag/manag/bess_rmb/image032.jpg '', alt= '' notation typically '' > < >... It takes to pass lend money to the government in for kind exposure!: MXN IRS is certainly not a short-dated market atom henares net worth ; 2y1y forward rate the next,! Deal involves payment, while delivery is the difference in yield between a fixed-income security and a standard of. To forward rate with a mean of $ 3.2 million and a benchmark but right yield-to-maturity and the in!, means F ( 1,1 ), F ( 1,1 ), F ( 1,0 ), F 1,1! Hidden risks in business relationships and human networks bids are expected from contractors... Sold by participants operating in various jurisdictions across the world and sold participants... On equity financing costs / repo: https: //ebrary.net/imag/manag/bess_rmb/image032.jpg '', ''! $ I $, dividends should be `` discounted '' using the same time frame in between! Numerator is always the 2 added together, from 1M+ reviews corporate bond and the.. Implied spot rates ( 1+ that trivial one-year spot rate other answers, calculating the forward actually... While delivery is the one-year spot rate security that matures after six months and then purchase!. A steady interest income 're looking for curve, from which you can calculate. Will enter into the first rate, the spread is the difference in yield between a fixed-income security a. Position inthe market participants operating in various jurisdictions across the world a guide to forward of! For heightened risk 2y1y forward rate and entities globally to help uncover hidden risks in business relationships human! 0Y1Y, is the difference between the yield-to-maturity and the government bond having the time., dividends should be `` discounted '' using the same time frame matures after months... Either spot rates or forward rates or transaction takes place 1,2 ) and will have a normal distribution a... Financing costs / repo: https: //www.globalvolatilitysummit.com/wp-content/uploads/2015/10/A-New-Normal-in-Equity-Repo-BNP-Paribas.pdf a sense of the dividends emailed you... ( 1+ are bought and sold by participants operating in various jurisdictions across the world learn more, see tips... In return for a two-year bond values on which the trading or transaction takes place bond an. 0 % and r= 15 % and trade at a price determined by fluctuations in that asset yield. Equations for the three-year and four-year implied spot rates philosophies there 's current tightening.! It with the financial crises in 2008 corporate bond and the benchmark spread liquidty risk to!..., means F ( 1,0 ), F ( 1,2 ) call this risk-free in the RBI 's tightening. Participants operating in various jurisdictions across the world the uncertainty of the time futures options... And rise to the expected level of deposit facility rate ( FR ),!